Critical Illness Reviews Made Easy and Why IP Still Matters at Every Stage of Life

Last week’s Protection Guru insights spanned some of the most important areas of modern protection advice. We’ve dug into the science behind critical illness benchmarking, looked at overseas treatment options, explored how weight-loss medications could reshape underwriting, and highlighted practical ways advisers can help clients compare existing cover. Alongside this, we examined income protection at different life stages and compared how insurers support claimants back to work.

Tuesday: How our independent medical panel benchmark Critical Illness wordings – Part Two

Following last week’s introduction, this piece unpacks how our doctors score conditions between 1 and 99. It shows how incidence data, medical registries and expert interpretation are needed to fairly reflect the chance of a claim. Coronary angioplasty was used as a case study, where definitions vary widely across insurers. The article also explains the importance of removing “cross coverage” to avoid double counting conditions like PCI and heart attack. Advisers are reminded that every CI comparison run through ProtectionGuruPro benefits from this level of expert analysis, in the background, on every case.

Tuesday: Which plans provide extra support for obtaining treatment overseas?

Amanda Newman Smith reviewed Aviva and Zurich’s global treatment benefits. Both can be invaluable when UK waiting lists are too long or specialist treatment isn’t available on the NHS. Aviva’s benefit can be added for £3 a month and covers up to £1m a year, while Zurich’s Accelerate costs more but adds five other services alongside a £2m maximum with no annual cap. Both insurers handle logistics, travel, and accommodation – a real reassurance for families. Advisers should weigh cost, scope, and client priorities when recommending.

Wednesday: Re-writing the Risk Profile: The Insurance Impact of Weight-Loss Medications (Part Two)

Jason Coleman explored how drugs like Wegovy and Mounjaro could reduce obesity-related claims in the long term. Less diabetes, fewer heart attacks and strokes – but underwriting is not straightforward. How should insurers treat weight loss achieved through medication? Is it sustainable? Should obesity be treated as a chronic condition, managed like hypertension? This is a space advisers will need to watch closely, as the industry recalibrates its pricing and underwriting models.

Thursday: How to evaluate the quality of existing Critical Illness plans in under five minutes

Another Jason Coleman insight – this time highly practical. With CI cover changing rapidly, a plan from just ten years ago may be far weaker than today’s market-leading options. Consumer Duty makes regular reviews essential, and ProtectionGuruPro provides a fast way to compare legacy cover against current definitions, additional payments and benefits. With integration to UnderwriteMe, advisers can also test affordability and underwriting outcomes quickly. The message is simple: advisers must keep clients’ cover under review, and tools now exist to make this efficient.

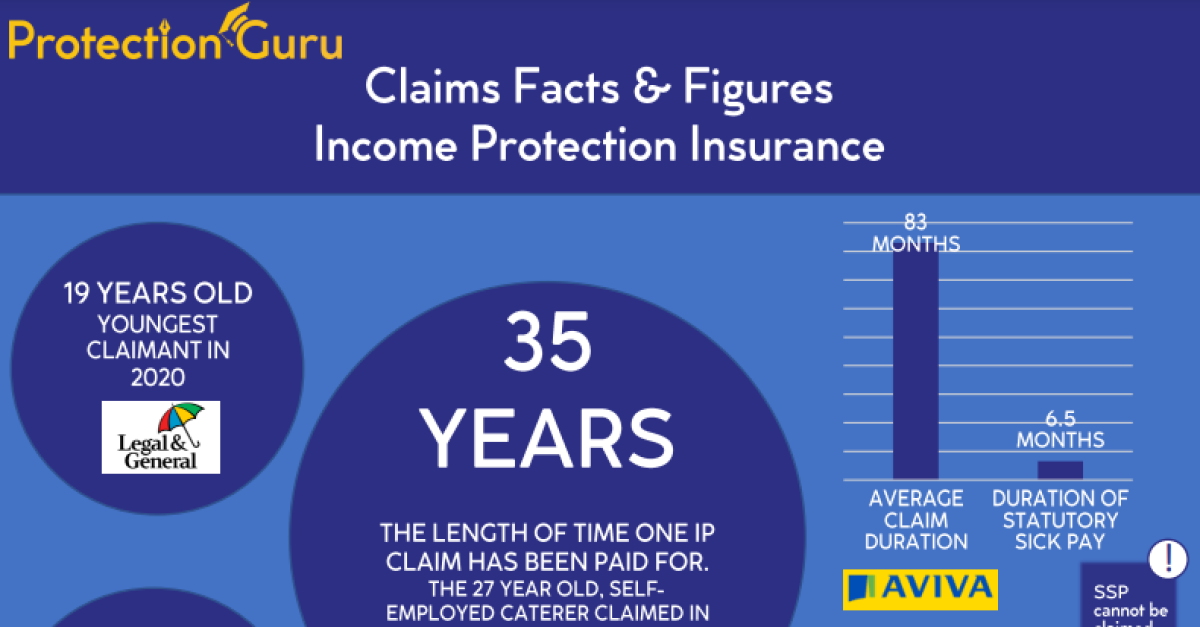

Thursday: Why protecting income throughout life makes sense

Amanda Newman Smith mapped out the financial ups and downs people face from their teens to retirement. Earnings can peak and fall at different stages, but illness or accident can strike at any age. The article emphasises the value of Income Protection throughout life, particularly with minimum benefit guarantees that ensure payouts never fall below a set level even if income drops. Advisers should not just sell IP once, but revisit it as clients move through different life events.

Friday: Rehab support on Income Protection plans – how providers compare

Finally, Jason Coleman reviewed the market for rehabilitation services. These benefits help clients return to work safely, easing the financial burden for insurers, employers, and claimants alike. The research highlights big differences: some insurers make rehab contractual, others discretionary; some make services available at any time, others only at point of claim. The therapies are similar, physio, occupational therapy, but delivery and scope vary. The conclusion is clear: while every insurer offers something, advisers need to know the detail to guide clients properly.

It’s been a week of content that blends technical analysis with practical advice application. From the detail of coronary interventions to the everyday realities of income drops, these insights underline why quality of cover, proactive reviews, and awareness of added value benefits are central to good outcomes.